Big thanks to Steven Thomas at Reports On Housing — his weekly data on Southern California supply, demand, and market speed is the backbone of this debrief. If you want the unfiltered numbers, subscribe to his report.

A Geopolitical Event Every Single Year

Take a quick look at the last few years:

- 2022 — Russia invades Ukraine

- 2025 — Tariff war kicks off

- 2026 — US-Iran conflict, with the Strait of Hormuz back in the headlines

It’s starting to feel like clockwork. Every year, some major geopolitical event drops into the middle of the economic conversation — and every year, we see the same pattern play out.

Phase one: shock. Financial markets jolt. Consumers freeze on big-ticket decisions. Anyone thinking about buying a home pumps the brakes.

Phase two: numbness. The headlines keep coming, but they stop hitting as hard. People get used to it.

Phase three: re-engagement. Life goes on. Attention shifts back to the things that actually run our lives — including housing.

We’re somewhere between phase two and phase three right now.

Where Mortgage Rates Were Headed Before Iran

Here’s the part that stings if you’re a buyer or seller this spring.

In March 2026, the 30-year fixed worked its way back down to around 6% — the lowest we’d seen in a long stretch. Momentum was building. Then the Iran conflict started, oil prices spiked, and the bond market reacted accordingly.

Right after the conflict began, the jobs report came in soft — over 100,000 fewer jobs than expected. In a normal cycle, that kind of weak labor data would have pulled mortgage rates down into the high 5s — something like 5.8%, territory we haven’t seen since August 2022. Instead, oil-driven inflation fears overwhelmed the rate-friendly jobs signal, and rates moved the wrong direction.

Without the Iran conflict, we’d very likely be looking at a dramatically better spring market right now — buyers locking in 5-handle rates, sellers seeing multiple offers again. Instead, the 30-year fixed is sitting around 6.25%–6.45% as of this weekend. The spring boost we should have gotten? Cancelled by oil and the Strait of Hormuz.

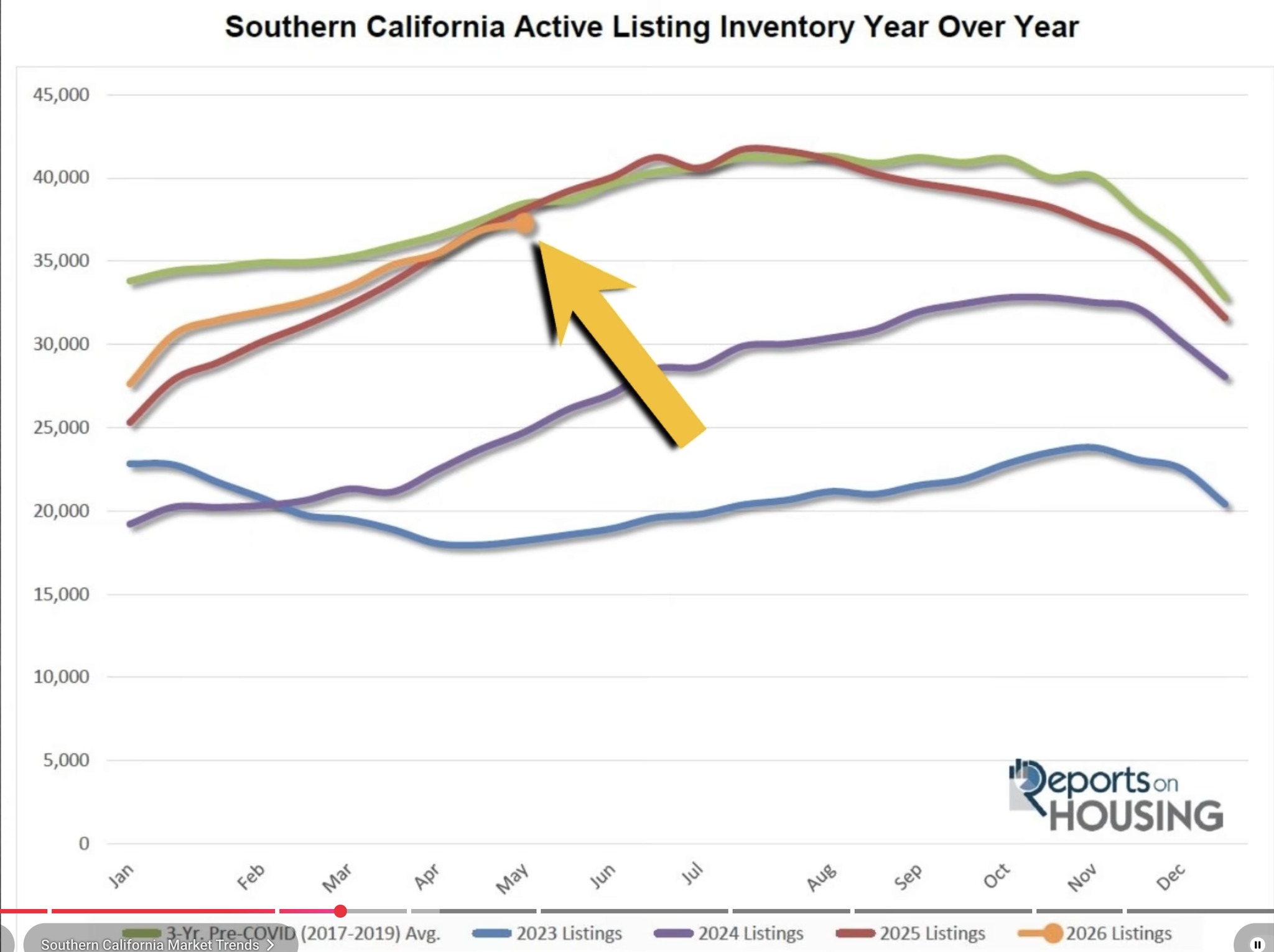

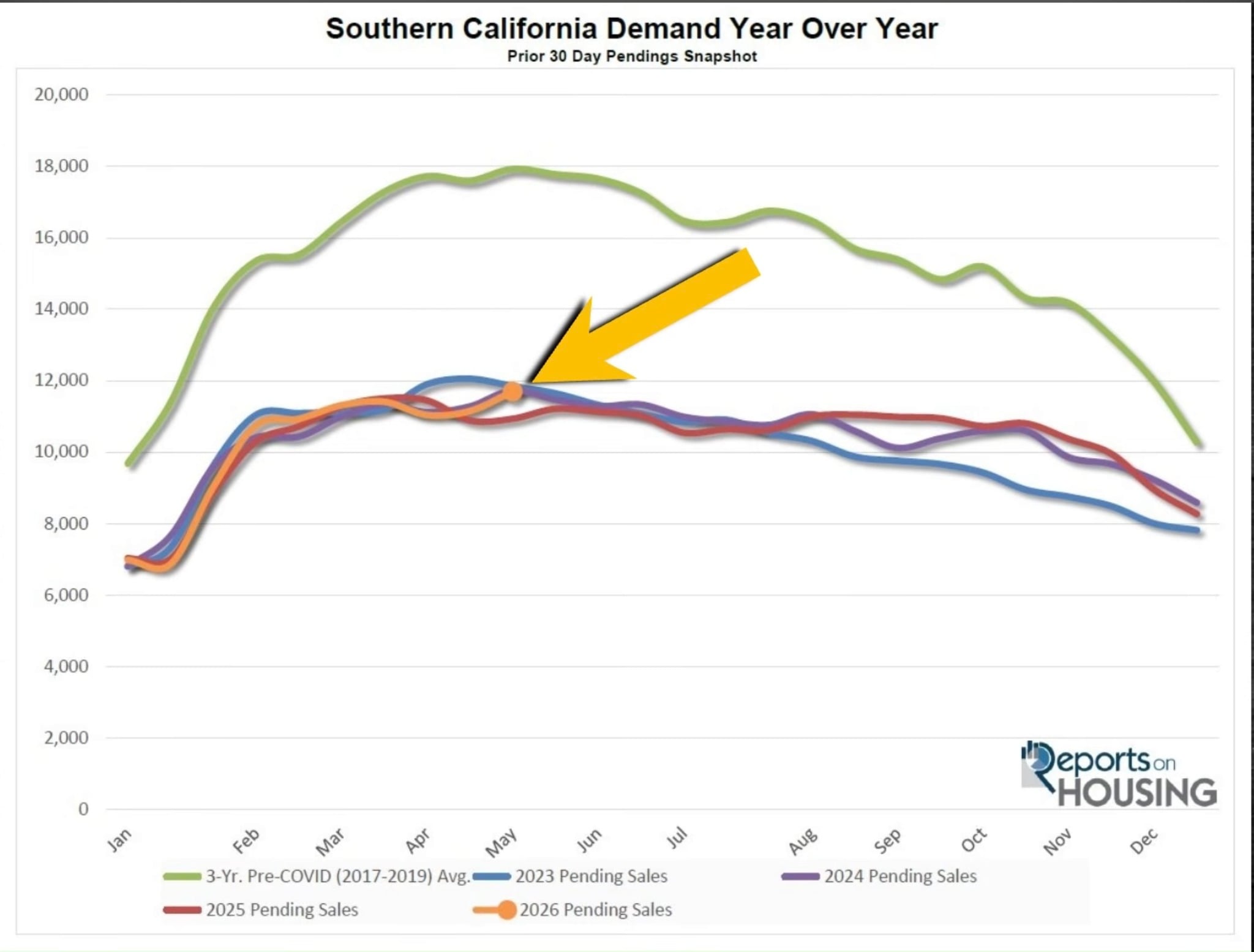

Southern California Snapshot

Despite the headwinds, the local market is telling an interesting story:

Inventory is lower than this time last year. Fewer homes are on the market.

Demand (pending sales) is slightly higher than last year. The seasonal peak usually lands in April or May. We’re looking at a later May this year, with a March dip that mirrors prior years — but overall demand is tracking similar to (slightly above) 2025.

Lower supply + similar-or-higher demand = market favors sellers a bit more than it did at this time last year.

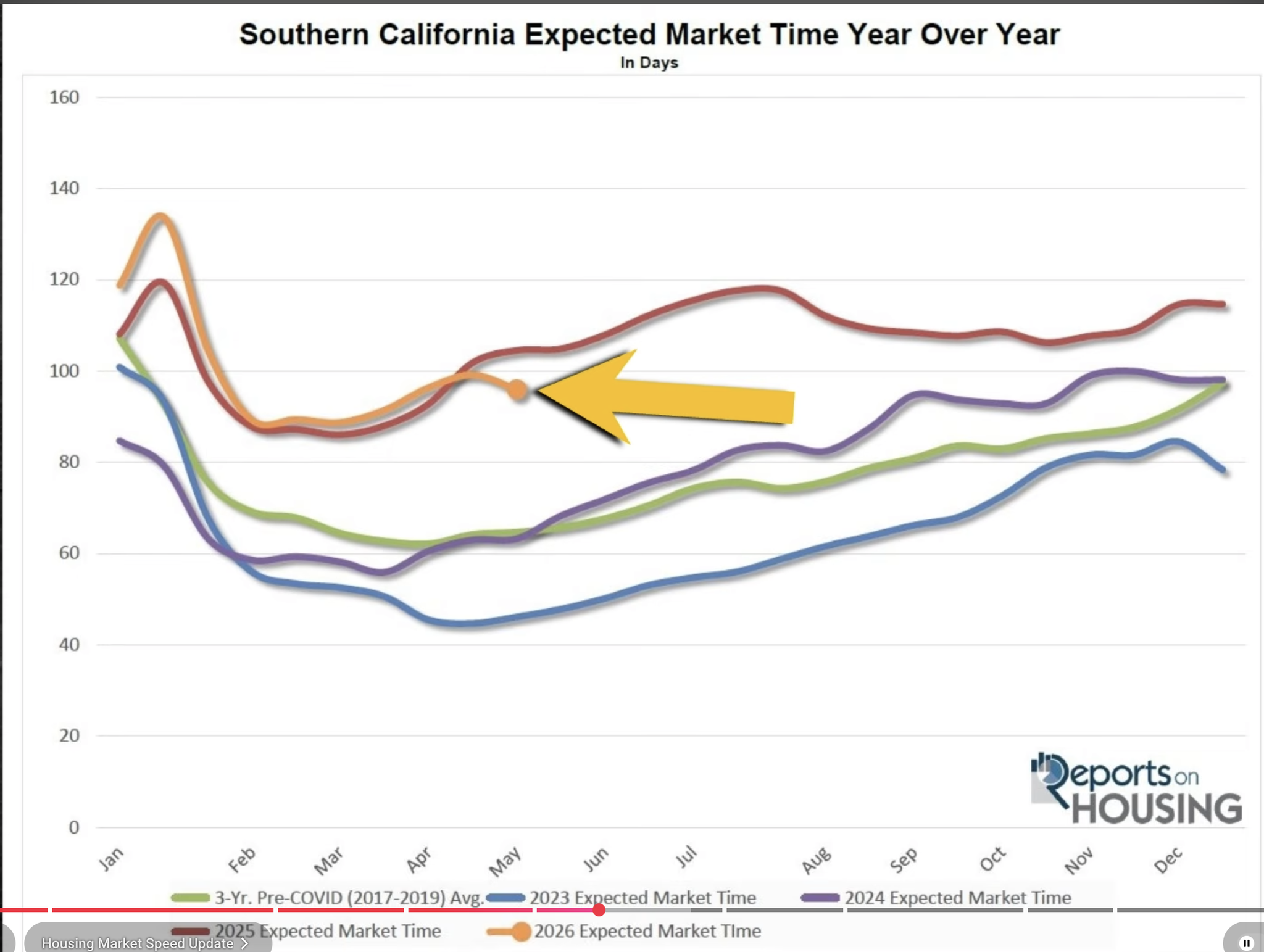

Speed of the Market

This is where the data gets a little surprising.

Homes are actually selling faster this year than last. Market speed has been dropping (faster sales = lower expected market time), whereas last year it was rising.

Had the Iran conflict not happened, we’d likely be looking at market speeds closer to 2024 levels — meaning a much hotter spring. We’re not there. But we’re moving faster than 2025, and that matters.

Where Are We Headed? The Tug of War

Here’s the macro picture as I see it heading into summer:

Pressure pushing rates DOWN:

- The longer the war drags on, the more volatile gas prices become — and prolonged volatility tends to weaken the broader economy.

- The labor market has been shrinking. If GDP softens, money flows into safe havens like mortgage-backed securities and Treasuries. When that happens at scale, rates come down.

Pressure pushing rates UP (or keeping them flat):

- April employment came in higher than expected. So did March. The headline numbers are still showing strength even as the underlying labor market thins.

- Iran-driven oil prices are feeding into inflation, which the Fed cannot ignore.

The Fed’s two jobs are maximum employment and price stability. They want to cut rates to support a weakening economy, but they need to hold rates to keep inflation in check. Right now those two mandates are pulling in opposite directions — a classic tug of war between a softening job market and energy-driven inflation.

What About the New Fed Chair?

Jerome Powell’s term ends May 15, 2026 — just a few days from now. Kevin Warsh is in the pipeline to succeed him. Whoever is running the Fed at the next meeting is unlikely to be in any hurry to cut as long as the Iran conflict keeps energy prices elevated. Cutting into an inflationary shock is the one thing a new chair really doesn’t want to do out of the gate.

Bottom line on rates: As long as the 30-year fixed stays north of about 6.25%, the housing market is going to feel a little frozen. Buyers stretch. Sellers wait. Transactions get done, but slowly.

What This Means for You

If you’re a seller: Inventory in Southern California is still tight and homes are moving faster than last year. The market is leaning your way more than it did 12 months ago. Pricing right and presenting well still wins — and it wins faster than it did in 2025.

If you’re a buyer: Rates are frustrating, but the worst thing you can do is wait for a perfect rate that may not arrive on the timeline you want. Marry the house, date the rate. If a property fits your life and your budget at 6.4%, refinancing later is a real option. Sitting out the market while prices in OC continue to grind sideways-to-up isn’t free either.

If you’re watching from the sidelines: Pay attention to two things — oil/gas prices and the next jobs report. Those are the two levers most likely to move mortgage rates between now and the end of summer.

Thinking about buying or selling in Orange County? I’d love to talk through what this market means for your specific situation.

Jack Ma, REALTOR®

Century 21 Masters | DRE #01869426

(909) 610-5188

Market data and analysis credit: Steven Thomas, Reports On Housing

Check out this article next